National Electronic Funds Transfer is a vital component of the banking system and financial machinery in India. It has enhanced the efficiency and speed of banking transactions in India. As the most widely used payment mechanism of individuals and companies, understanding NEFT in the era of digital transformation is crucial.

In this article, we delve into the intricacies of NEFT transactions in India, exploring its mechanisms, benefits, and impact on the banking system and the economy at large.

Get Free Trading Calls from SEBI Registered Experts

What is NEFT?

NEFT stands for National Electronic Funds Transfer. It is an electronic payment system in India that permits one-to-one fund transfers in India. It enables individuals, corporations, or firms to electronically transfer funds from one account to another across the country. It operates on a deferred settlement basis or payments are deferred to be settled on a later date.

RBI started NEFT in 2007. It settles transactions in half-hourly batches and is available 24/7 throughout the year.

How Does NEFT Work?

NEFT operates through a secured and standardized process. Here is the step-by-step process of the working of NEFT.

- Firstly, the sender initiates the transaction by submitting a fund transfer request. The sender can submit through internet banking, mobile banking, or by visiting a branch of the bank.

- The sender’s bank verifies the request details for the translation and authorizes it. Then, the bank debits the specified amount with its charges from the sender’s account.

- The sender’s bank prepares and sends the message to the NEFT service center, which is its pooling center.

- The sender’s bank sends details to the RBI’s NEFT system, which acts as the central hub. The RBI NEFT system then forwards the request to the receiver’s bank through a secure channel.

- Once the transaction is requested, the receiver’s bank processes the transfer and credits the receiver’s account with the specific amount transferred.

- NEFT transactions are settled at predefined intervals throughout the day. During the settlement process, the transactions are balanced out between the banks involved, making sure everything adds up correctly.

- The sender and receiver get messages when the transaction is completed. The message will include the transaction reference number, amount transferred, and transaction status.

NEFT Timings and Charges

As per the recent regulations, you can perform transactions 24/7 throughout the year, including public holidays. However, the actual crediting of the fund to the recipient’s account may vary depending on the working hours of the recipient’s bank.

Most banks levy nominal fees for outward NEFT transactions, which vary based on factors such as transaction amount and customer category. However, inward NEFT transactions are generally free for the recipient.

RBI has limited the maximum fees banks can charge from customers. The following table will show the maximum fees banks can charge for transactions.

| Transaction Amount | Maximum Fees |

| Up to ₹10,000 | ₹ 2.50+GST |

| ₹ 10,000- 1,00,000 | ₹ 5+GST |

| ₹1,00,000- 2,00,00 | ₹ 15+GST |

| Over ₹ 2,00,00 | ₹ 25+GST |

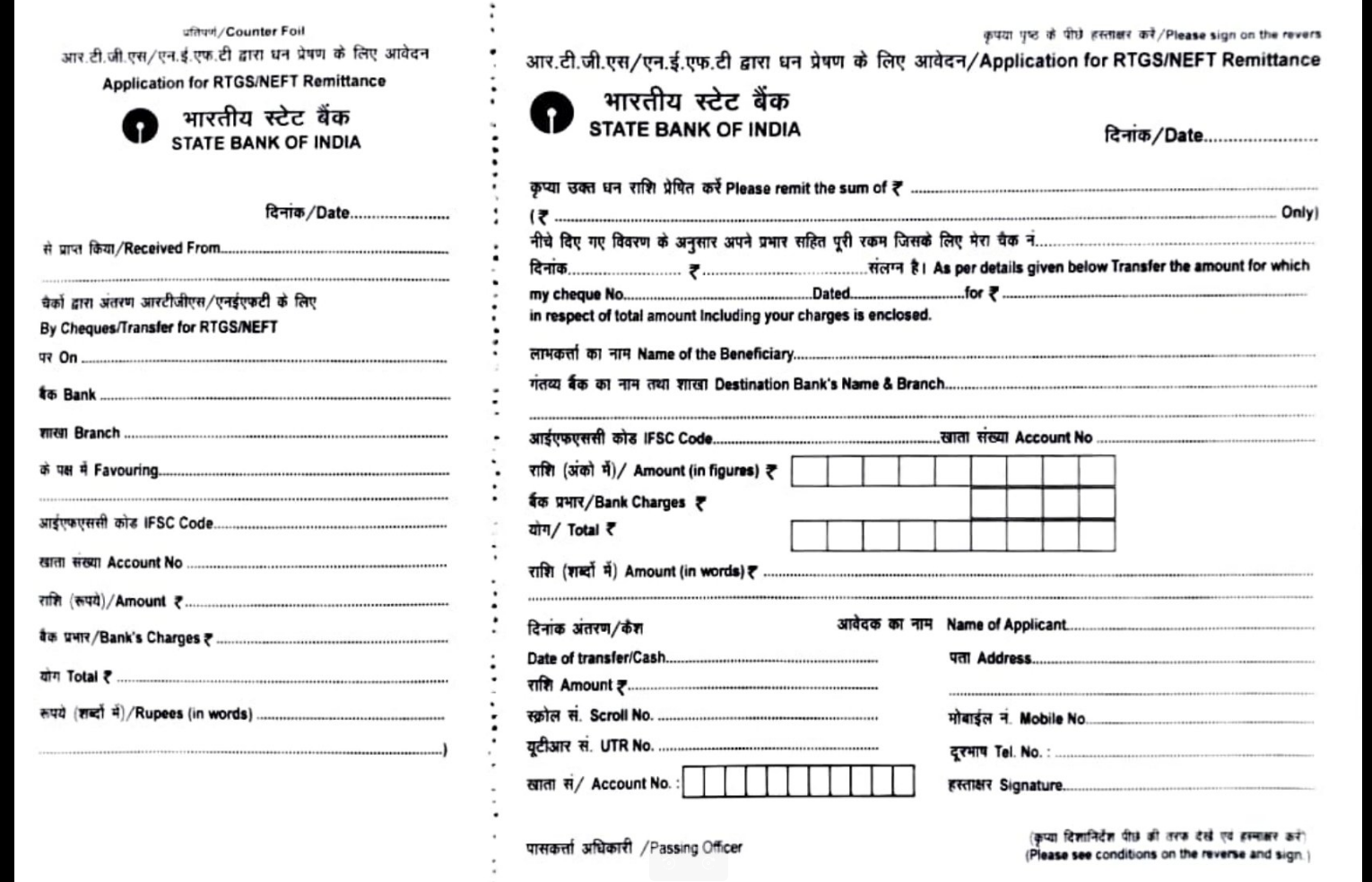

NEFT Form

To do an offline transaction at the bank, you need to fill out a form. You need to fill out your name, account number, and address along with beneficiary details.

How Do You Make a NEFT Transfer?

Let us see the step-by-step process to make an NEFT transfer below:

- Visit the website or the mobile application of the bank where you have your account.

- Log in to the net banking portal or application using your username and password.

- Fill out the account number, name, IFSC, and account type, and add beneficiary.

- Go to the payment section of the website to initiate a transaction and choose NEFT as the payment type.

- Choose the account from which you want to send money.

- Select the beneficiary, enter the amount you wish to transfer, and click on Submit.

Details Required to transfer Funds Through the NEFT system

To initiate a transaction, you need the following details:

- Name of the beneficiary

- Name of the beneficiary’s bank and branch.

- IFSC Code of Beneficiary

- Account type and account number of beneficiaries.

Benefits of Using NEFT for Transaction

NEFT provides several advantages to individuals and businesses, which led to its popularity and widespread usage.

- NEFT is one of the convenient modes of transaction. It provides a hassle free avenue to transact funds from the comfort of their home or office through digital channels

- Individuals or businesses can transfer funds to accounts 24/7 and the whole year

- There is no maximum or minimum amount of transaction in the case of NEFT

- There is no limit from the RBI’s side regarding the daily limit

- You can transfer funds to an NRI or NRO account

- You can send money to Nepal

- Someone without a bank account can also do NEFT transactions

- NEFT transactions usually levy lower fees compared to other electronic payments. Hence, it is a cost effective option for transferring funds, especially transactions of large amounts and volume

- NEFT transactions adhere to strict security protocols and encryption standards, ensuring the confidentiality of financial information throughout the transaction process.

- NEFT system can be used for various other transactions like payment of credit card dues, payment of loan EMI, etc.

Frequently Asked Questions About NEFT

What is the full form of NEFT?

National Electronic Fund Transfer

What is UTN?

A unique Transaction Number is a reference number provided by the sender’s bank account for every transaction.

Is there any limit to the amount that can be transferred using NEFT?

No. There is no upper limit nor lower limit to the transaction amount through NEFT.

What is the IFSC code?

Indian Financial System Code is an 11-digit code that uniquely represents a branch of a bank participating in NEFT transactions.

Do all banks in India participate in NEFT transactions?

No. The list of banks and their branches participating in NEFT transactions is available on the RBI website. https://rbi.org.in/Scripts/bs_viewcontent.aspx?Id=2009

Is there a limit to the amount that can be transferred through NEFT transactions?

No. RBI does not impose any restrictions on the maximum amount of transactions through NEFT. However, individual banks may place limits on the transaction amount with the approval of their board.

Can a person without a bank account transfer funds through NEFT transactions?

Yes. A person who does not have a bank account can transfer funds to a beneficiary with a bank account. They can do so by depositing cash to a NEFT-enabled bank account by providing details such as name, address, etc. However, the amount is restricted to 50,000 per transaction.

Whom should I contact to raise a complaint related to the NEFT transaction?

You can approach the grievance redressal cell of your bank with the details of the transaction.